LIFE INSURANCE | Term Vs. Permanent Life Insurance

Less than half of middle income earners age 25 to 64 own individual life insurance, according to LIMRA, which keeps close tabs on the life insurance industry. In the same survey, 44% of those who didn't have it said they needed it.1

When considering life insurance, one of the most important factors to understand is the difference between term and permanent insurance. Here’s an inside look at both.

Term or Perm?

Term life insurance is temporary; it provides a death benefit for a specific term, such as 10, 20, or 30 years. Unlike other types of life insurance, it does not accumulate a cash value. If the policyholder dies during that term, his or her beneficiaries receive the benefit from the policy. When the contract ends, so does the coverage.

This limited term leads to term life insurance’s main advantage: price. Generally, term life insurance costs less than permanent life insurance, especially if the purchaser is younger. This has the potential to free up funds for other household expenses.

Permanent insurance remains in place as long as the policyholder makes payments. In addition, permanent policies are designed to build up “cash value,” a cash reserve that accumulates with the policy. Typically, this cash reserve pays a modest rate of return. However, the policyholder has limited access to the funds.

Which Should You Choose?

Term life insurance can be designed to provide protection against upcoming expenses, such as putting children through college. Permanent life insurance, on the other hand, can be more useful for covering long-term financial needs, such as estate planning.

Many people find that they have a combination of short- and long-term needs. In such circumstances, it may be prudent to have both types: a basic level of permanent life insurance supplemented by a term policy. A review of your situation may help determine what type of life insurance is appropriate.

Several factors will affect the cost and availability of life insurance, including age, health and the type and amount of insurance purchased. Life insurance policies have expenses, including mortality and other charges. If a policy is surrendered prematurely, the policyholder also may pay surrender charges and have income tax implications. You should consider determining whether you are insurable before implementing a strategy involving life insurance. Any guarantees associated with a policy are dependent on the ability of the issuing insurance company to continue making claim payments.

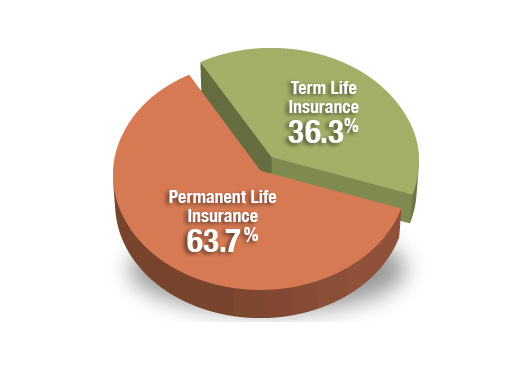

Term or Perm?

In 2013, (the most recent year for which statistics are available), people purchased more permanent life insurance policies than term life insurance policies.

Source: American Council of Life Insurers, 2014

1. LIMRA, 2014

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. This material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG, LLC, is not affiliated with the named broker-dealer, state- or SEC-registered investment advisory firm. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Copyright 2015 FMG Suite.

LIFE INSURANCE

Fast Fact: More than 50% of the uninsured say that additional living expenses, such as cable, Internet, and cell phone costs prevent them from buying life insurance.

Source: Source: LIMRA, 2014

Avantax affiliated advisors may only conduct business with residents of the states for which they are properly registered. Please note that not all of the investments and services mentioned are available in every state.

Securities offered through Avantax Investment ServicesSM, Member FINRA, SIPC. Investment advisory services offered through Avantax Advisory ServicesSM. Insurance services offered through an Avantax affiliated insurance agency.

The Avantax family of companies exclusively provide investment products and services through its representatives. Although Avantax Wealth ManagementSM does not provide tax or legal advice, or supervise tax, accounting or legal services, Avantax representatives may offer these services through their independent outside business.

This information is not intended as specific tax or legal advice. Please consult our firm and your legal professional for specific information regarding your individual situation.

Content, links, and some material within this website may have been created by a third party for use by an Avantax affiliated representative. This content is for educational and informational purposes only and does not represent the views and opinions of Avantax Wealth ManagementSM or its subsidiaries. Avantax Wealth ManagementSM is not responsible for and does not control, adopt, or endorse any content contained on any third-party website.